Growth and ROIC

Sometimes growth can be predictable

It is common knowledge that corporate growth is fleeting.

Competitive theory states that once a firm takes advantage of a lucrative market, competition soon arises to even the playing field. Over the long term, growth stalls and returns on the invested capital decline to a company’s cost of capital - neutralizing economic profits.

The data seems to back up this theory.

British economist I.M.D conducted a study in the 1960s that found no relationship between growth rates achieved by any company in one five-year period and those achieved in the next five years.

In 2015, Credit Suisse's HOLT researchers - Bryant Matthews and David Holland - found that growth rates are the plaything of chance. The two concluded, "Growth rates show little persistence, are excessively volatile, and mean-revert rapidly over the medium-term toward 5% real asset growth."

This mean reversion is often cited as a result of rising competition.

Despite the evidence, investors repeatedly overestimate companies' expected growth rates to justify their valuations. During 2009 and 2014, equity analysts overestimated earnings growth for the Stoxx 600 index by an average of more than 10% per annum.

Are all businesses doomed to slow?

While the samples for these studies included a broad universe of companies, a subset of businesses seem to be able to defy competitive theory.

These businesses have managed to build and sustain competitive advantages through intangible assets or scale efficiencies.

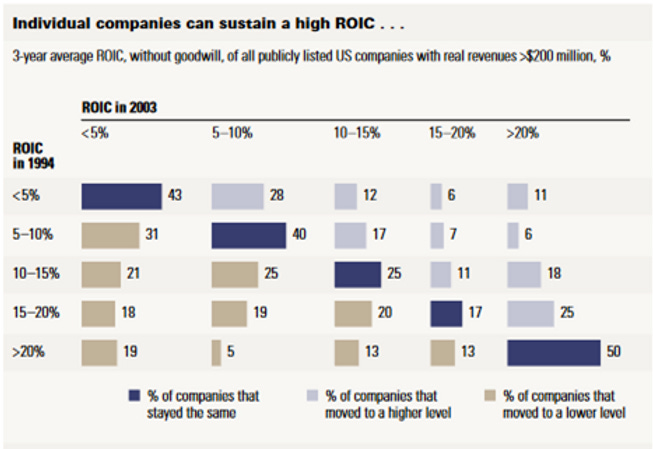

To identify these businesses, we can use what we deem to be the most important investing metric – return on invested capital. A study by Mckinsey & Company between 1994 and 2003 found that individual companies with high levels of ROIC tend to hold on to their advantage.

Source: McKinsey & Company

"The chart looks at the probability that a company will migrate from one level of ROIC to another over the course of a decade. A company that generated an ROIC of less than 5 percent in 1994, for instance, had a 43 percent chance of earning less than 5 percent in 2003. As the exhibit shows, low and high performers alike demonstrate consistency throughout the 40-year period. Companies with an ROIC of 5 to 10 percent had a 40 percent probability of remaining in the same group ten years later; companies with an ROIC of more than 20 percent had a 50 percent probability." - McKinsey & Company

If these high-quality businesses have ample reinvestment opportunities, growth rates can hold for an abnormal period of time because each dollar invested creates more than a dollar of earnings.

Credit Suisse's HOLT researchers agreed that there is a strong relationship between higher cash returns on investment and higher earnings growth sustainability. Furthermore, a consistent high-return on capital business provides a better base for earnings growth predictability.

Consistency is key. Young businesses experiencing hypergrowth and extraordinary returns may only do so for a short period. Similarly, companies without competitive advantages require more and more capital investment to maintain earnings growth rates.

Capital efficient firms with decades of staying power are a different class and our preferred investment choice. These quality companies provide both earnings consistency and low forecast error rates.

They may not reward investors with high double-digit annual returns, but slow and steady incremental shareholder value creation over time can accumulate to a wonderful result.

References

Lawrence A Cunningham. Quality Investing: Owning the best companies for the long term. Harriman House. Kindle Edition.

Bryant Matthews and David A. Holland, ‘Prepared for Chance: Forecasting Corporate Growth’, February 2015.

Bing Cao, Bin Jiang, and Timothy Koller. “Balancing ROIC and growth to build value”. March 2006.